In the years leading up to the acquisition of my company, I developed an interest in the shareholder primacy versus stakeholder primacy discussion. I read transcripts of the Milton Friedman/John Mackey discussions, and on my long commute I listened to countless podcasts with hosts and participants debating the issue. I attended a conference where Raj Sisodia was the keynote speaker, advocating for stakeholderism. I read the books, ‘Conscious Capitalism,’ ‘Conscious Leadership,’ and ‘Firms of Endearment.’ I thought deeply about the issue – contextualizing it against the backdrop of my company and my experience as an entrepreneur. In my final years as the company’s CEO, I witnessed an emergence of stakeholderism, within my company, in response to a change of perspective and a transition to more conscious leadership. The shift to a conscious, stakeholder-oriented culture yielded positive results.

Despite the positive results, I struggled with the debate because I could not see shareholder primacy and stakeholder primacy as dichotomous. I view shareholders as a subset of stakeholders because they are affected by the transactional process. The better framing of the argument was short-term versus long-term shareholderism. When we place our attention on the entirety of our stakeholders, we serve our shareholders in the long term at the expense of short-term results. Conversely, when we focus disproportionately on our shareholders, we serve those shareholders in the short term at the expense of long-term results and sustained success. In company dialogue, we expressed the same debate as ‘trading brand for profit versus trading profit for brand.’

Taking either position supports the importance of serving shareholders – the difference being whether they are best served in the short or long term. This distinction does not change the essence of the argument; it simply reframes the argument in a way that narrows the debate in favor of the current stakeholder perspective. Deferring gratification is the essence of maturity. From this perspective, stakeholder primacy is more conducive to the maturing of an organization. As our organizations mature, we can increasingly focus on their stakeholders. At the same time, doing so fosters organizational maturity. A mature organization better serves its shareholders in the long term.

With the shareholder/stakeholder debate reframed as a short-term, long-term issue, there may be a more relevant discussion regarding the ‘primary purpose’ of business. Rather than debating the primary purpose of business as serving shareholders or stakeholders, perhaps the debate should be serving Wall Street or serving Main Street – or the valuation of our companies versus the value they bring to the marketplace. We should consider that a business’ ‘primary purpose’ is to add value to the marketplace. Adding value for shareholders is a result of adding value to the marketplace. Adding value for stakeholders is a method by which we bring this value to the marketplace.

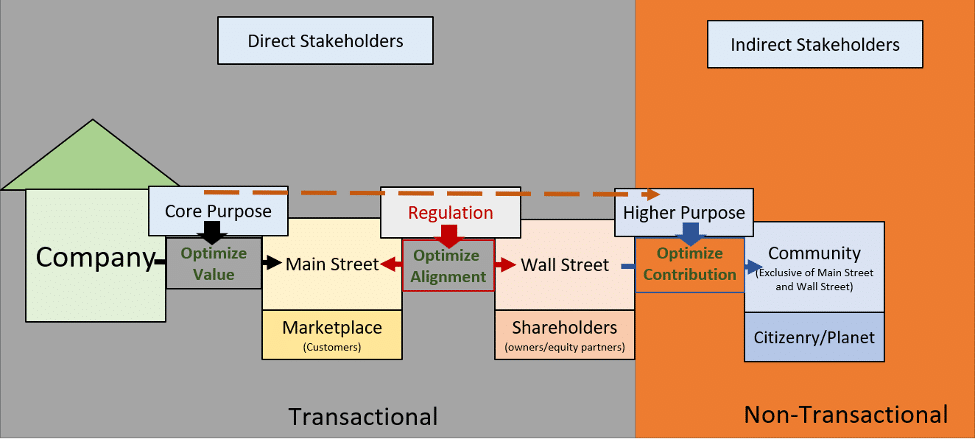

The ecosystem of the business transaction includes the shareholders, the marketplace, regulatory entities, and the stakeholders. For purposes of this model, let’s call the shareholders ‘Wall Street’ (we are not making a distinction between publicly traded and privately held companies), and let’s call the marketplace ‘Main Street’ (we include all businesses and business transactions – not just retail). The regulatory entities are responsible for legislation and regulation (this includes local, State, and Federal regulations, statutes, and laws – and may include internal policy and some functions of The Board of Directors). Finally, the stakeholders are anyone affected by the transaction (including shareholders).

How a business serves Main Street (adds value to the marketplace) within the transactional ecosystem is its ‘Core Purpose.’ A fully discovered and clearly communicated Core Purpose is essential to organizational health. The people affected within this transactional ecosystem are the ‘Direct Stakeholders.’ These typically are customers, employees, vendors, landlords, lenders, etc. How a business adds value outside of the transactional ecosystem is its ‘higher purpose.’ The distinction between Core Purpose and higher purpose is important: A Core Purpose is essential – a higher purpose is not. The people affected outside the transactional ecosystem – the higher purpose, are ‘Indirect Stakeholders.’

With the primary purpose of business being to add value to the marketplace (serving Main Street), the shareholder benefit (serving Wall Street) should be a product of how well the business fulfills its primary (Core) purpose. Pragmatically tethering Wall Street to Main Street – or linking shareholder value to the value brought to the marketplace, is a responsibility of the regulatory entities (internal and external). When the value brought to Main Street is optimized, stakeholders (including shareholders) are best served in the long term.

The tethering of Wall Street to Main Street (shareholder value linked to the value brought to the marketplace) is the transactional ecosystem. This ecosystem is manifest in the business’ Core Purpose. A secondary ecosystem is manifest in the business’ higher purpose. This is a non-transactional ecosystem. The non-transactional ecosystem is altruistic – it is where we find a company’s CSR initiatives. (A distinction between CSR and ESG may be that the philanthropy and volunteerism included in CSR initiatives are part of the non-transactional ecosystem, while ESG compliance is more likely to be part of the transactional ecosystem). This non-transactional ecosystem is where a company chooses to be a good citizen of society or the planet by adding value outside the transaction. The non-transactional ecosystem is subordinated to the transactional ecosystem. The resources a company can commit to its non-transactional ecosystem are proportionate to the effectiveness and efficiency of its transactional ecosystem. So, again, the tethering of Wall Street to Main Street through policy, regulation, and legislation serves both purposes. When effectively tethered, the more value a company brings to the marketplace (its Core Purpose), the better it can serve its higher purpose and its shareholders in the long term.

Viewing these two ecosystems (transactional and non-transactional) as exclusive is deficient. It is reasonable to think – and there are data to support that direct stakeholders within the transactional ecosystem value the higher purpose of the non-transactional ecosystem. Employees and customers prefer working for and buying from businesses with a higher purpose – or non-transactional ecosystem. Further, public companies that have a higher purpose or a non-transactional ecosystem may trade at higher multiples because of investor sentiment (this is ironically an untethering of Wall Street and Main Street). This non-transactional higher purpose adds value to the transactional ecosystem.

Summary

In summary, fundamental to the concept of purpose is that rather than viewing ‘the’ primary purpose of business as optimizing value for shareholders – or for stakeholders, we can reframe the shareholder/stakeholder debate as short-term versus long-term intent. Instead, the primary purpose of business is to add value to the marketplace. The transactional ecosystem is best-served long-term when regulation tethers shareholder value to the value the company or entity brings to the marketplace. This is not to say that ‘financial vehicles’ by which share prices can be raised or accelerated (i.e., stock buybacks, derivatives) don’t have value – but rather that usurping the Core Purpose of business by diluting value to the marketplace is unproductive in the long-term. We should subordinate these opportunities to add value for shareholders to the principle of adding value to the marketplace (including consideration for future value) through the goods and services provided. This subordination is the responsibility of effective regulation (both internal and external).

From there, we can fulfill the moral imperative of a higher purpose, proportionate to how efficient and effective our transactional ecosystem is – while, at the same time, deriving incremental benefit for the transactional ecosystem, i.e., improved financial performance that better serves the shareholders over the long term.